SP500 LDN TRADING UPDATE 26/2/26

SP500 LDN TRADING UPDATE 26/2/26

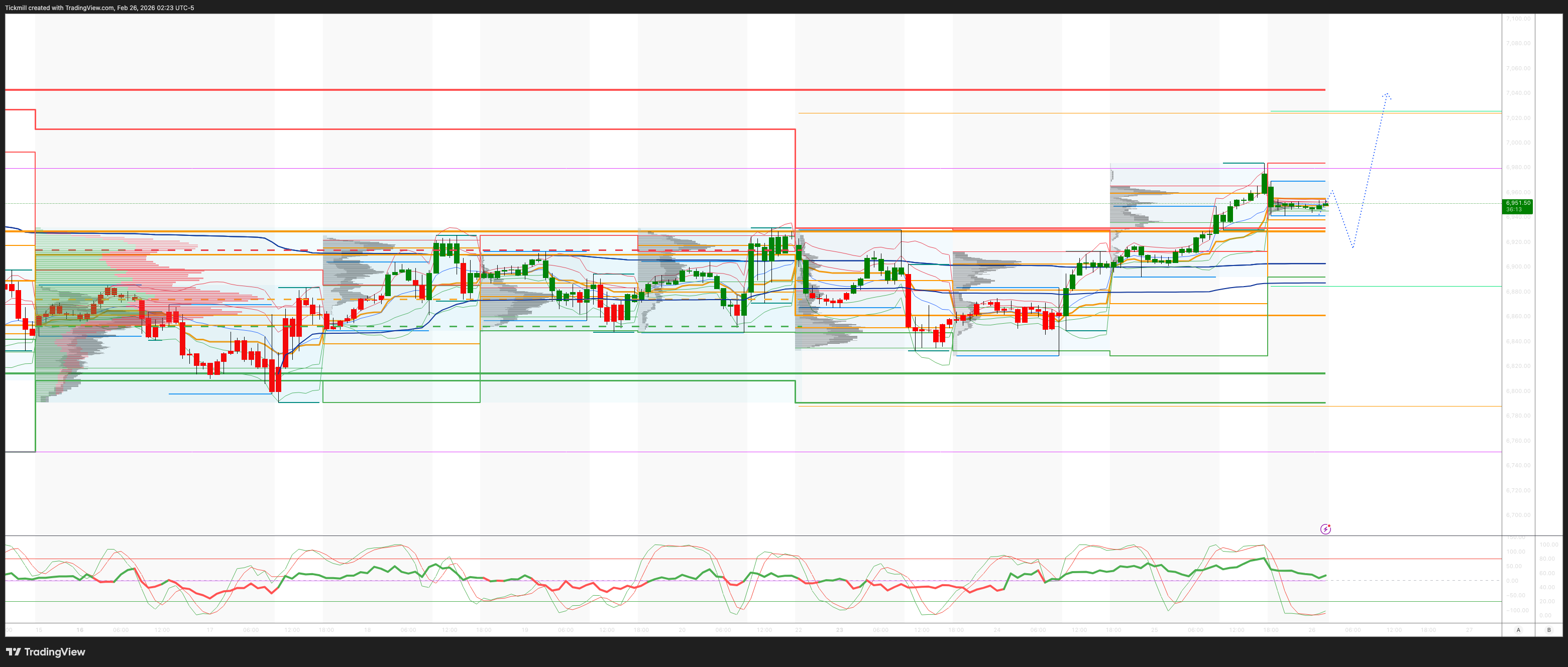

WEEKLY & DAILY LEVELS

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6925/15

WEEKLY RANGE RES 7046 SUP 6906

FEB EOM Straddle indicates a range of 214.6 points, suggesting a monthly FEB range of [6725, 7154].

FEB OPEX Straddle shows a range of 213.6 points, leading to an OPEX to OPEX range of [6726, 7154].

MAR QOPEX Straddle offers a range of 368.55 points, resulting in a range of [6466, 7203].

The range from DEC2025 OPEX to DEC2026 OPEX is 945 points, providing a range of [5889, 7779].

DAILY VWAP BULLISH 6876

WEEKLY VWAP BEARISH 6928

MONTHLY VWAP BULLISH 6865

DAILY STRUCTURE – ONE TIME FRAMING HIGHER - 6929

WEEKLY STRUCTURE – BALANCE 7031/6801

MONTHLY STRUCTURE – TBC

DAILY RANGE RES 7037 SUP 6914

GAMMA FLIP 6898

TRADES & TARGETS

LONG ON REJECT/RECLAIM WEEKLY BULL BEAR ZONE TARGET DAILY RANGE RES

SHORT ON REJECT/RECLAIM OF WEEKLY RANGE RES TARGET WEEKLY BULL BEAR ZONE

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Tech Tape’

S&P rose +81bps, closing at 6,946 with a MOC of $600m to BUY. NDX gained +141bps, ending at 25,329; R2K increased +41bps to 2,663, while the Dow climbed +63bps to 49,482. Trading volume reached 17.5 billion shares across all US equity exchanges versus the YTD daily average of 19.26 billion shares. VIX dropped -849bps to 17.86, WTI Crude slipped -24bps to $65.47, US 10YR edged up +2bps to 4.05%, gold rose +29bps to 5,159, DXY fell -14bps to 97.70, and Bitcoin surged +8% to $69,200.

Markets rallied higher in a "cover-the-news" style, particularly across the Software and broader AI-at-risk sectors. Software stocks advanced +5%, with WDAY recovering to finish +2% after initially dropping 10% overnight due to a weaker '26 guide. The rally was supported by a more favorable Anthropic event (AI partnership with Software incumbents rather than displacement) and growing investor pushback against negative sentiment in blogs like Citrini’s. Flows were orderly, reflecting supply abatement and hedge fund covering rather than significant new buyer activity.

AFTER HOURS: NVDA rose +4%, returning above $200 following a strong beat versus consensus for the quarter and guiding the April quarter well ahead of expectations ($76.4–79.5bn vs. $73bn consensus). Positioning was rated 8/10, indicating solid holdings despite some reductions. SNOW climbed +6%, guiding '27 product revenues above street expectations. CRM fell -3%, citing second-half weighted organic growth guidance and announcing a $50bn buyback (28% of market cap). NTNX surged +20% as AMD announced plans to purchase $150mn in NTNX stock under a new partnership. TTD dropped -15% due to 4Q revenue growth of +14% y/y and a disappointing 1Q revenue guide ($678mn vs. $688mn consensus). ZM slid -1% after a slight revenue beat (+4.8% y/y cc), with Enterprise revenues up +7.1%, FY revenue guidance above street expectations, but EPS guidance below. ARRY fell -16% due to FY outlook missing consensus. HEI declined -9% after Q1 EPS of $1.35 beat consensus ($1.28), though revenue ($1.18bn vs. $1.17bn consensus) and EBITDA ($312mn vs. $315.6mn consensus) were in line. FTAI dipped -7.5% following an EPS miss, with earnings disappointment coming after a strong performance (+7% yesterday, +53% YTD).

DERIVATIVES: A busy day on the desk as the S&P realized its full implied move within the first 20 minutes of the session. In S&P and Nasdaq, skew relaxed in the front end, remaining mostly unchanged further out. Volatility floated higher during the rally but ultimately came in, particularly on the front end. Two significant VIX trades were noted: a buyer of 100k contracts for VIX Jun 22 calls and another buying ~70k contracts for VIX Mar 27 calls outright. Continued interest in year-end SPX binary call spreads was observed, with a customer purchasing nearly 30k of the 31Dec 8090/8190 call spread (around 40m vega per leg). Additionally, NDX saw buyers of downside protection in the 1–3m tenors. In micro trading, the desk was active in TMT and software, observing marginal skew toward upside flows, particularly in 1–3m NVDA upside. The S&P straddle through the week closed at 99bps.

PRIME – SOFTWARE BOUNCE: The recent rebound in Software and select IT Services stocks appears to have near-term potential due to positioning and technical factors. Software and IT Services were the #1 and #2 most shorted US industries on the Prime book as of February 24th, across daily, weekly, monthly, and YTD metrics. Short exposure (as a percentage of total US single stock gross MV) has climbed sharply to its highest recorded level since 2016, while long exposure in US Software & Services stocks has dropped to a record low. The aggregate long/short ratio in US Software & Services is now at 1.14 (down from 1.82 at the start of 2026 and a historical peak of 4.74). Hedge funds are underweight Software & Services stocks by -6.8 pts relative to the Russell 3000 index, marking the most underweight level on record (compared to -3.9 pts underweight

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!